IFRS16 lease accounting - what to record?

According to the provisions of IFRS16, several types of costs can be covered by leasing. In IFRS16, accounting applies to the amount of the lease liability, any other payments made prior to the contract's inception date, direct costs incurred by the lessee in connection with entering into the contract, as well as estimated expenses related to bringing a job or place in the company to its pre-lease condition, targeted for the period after the end of the contract. Assessing the value of a leased asset as a right to use it entails additional valuation under IFRS16 accounting.

There are three valuation models here, as described in IFRS16: the cost model, the revalued value model, and the hourly value model used for investment properties. Right-of-use assets are also valued taking into account their depreciation, in accordance with the provisions of IAS 36.

When complying with IFRS16, accounting is worth addressing in a comprehensive manner, taking inventory of all leases beforehand. It may turn out that IFRS16 leases will also cover other previously unclassified contracts. Next, accounting IT systems may need to be adapted to effectively account for subsequent contracts.

FAQ

How many contracts can the application support?

The ILA16 application can handle up to several dozen thousand leasing contracts. The number of supported contracts depends on the purchase plan. With the BASIC plan, it is up to 500 leasing contracts. Our clients include companies maintaining from several dozen to several thousand contracts.

In which purchasing plans is it possible to conclude an SLA?

The SLA (Service Level Agreement) applies to the Business, Enterprise and Existing Clients plans. The only package that does not include an SLA guarantee is the Basic package.

What external systems can the ILA16 application integrate with?

The leasing contract management application integrates with most ERP systems available on the market via Rest API. This option is available in the Business, Enterprise and Existing Clients purchasing plans.

Is there a maximum number of contracts that the application can support?

The ILA16 application has no limit on the number of contracts that can be processed on an ongoing basis. Currently, for one of our clients, the application supports over 18,000 contracts in the system.

What is the maximum number of companies to use in the application?

There is no upper limit on the number of companies for which we enter contracts in the system.

Is it possible to adjust the categorization of contracts?

Yes. According to the client's needs, we modify the appropriate hierarchies related to contracts to make navigation in the system as simple and quick as possible for users.

How does the application allow you to manage contracts settled in currencies other than PLN?

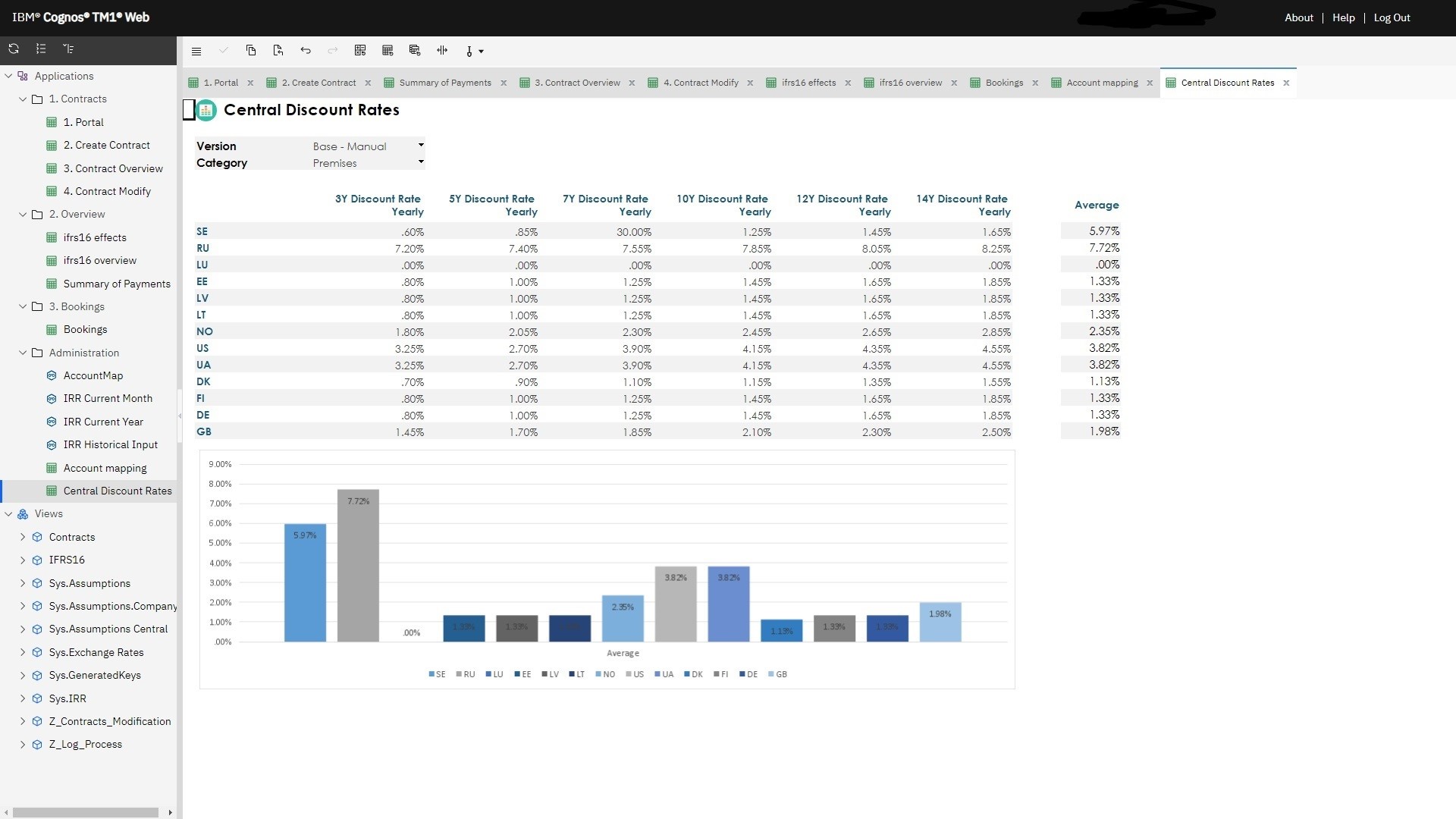

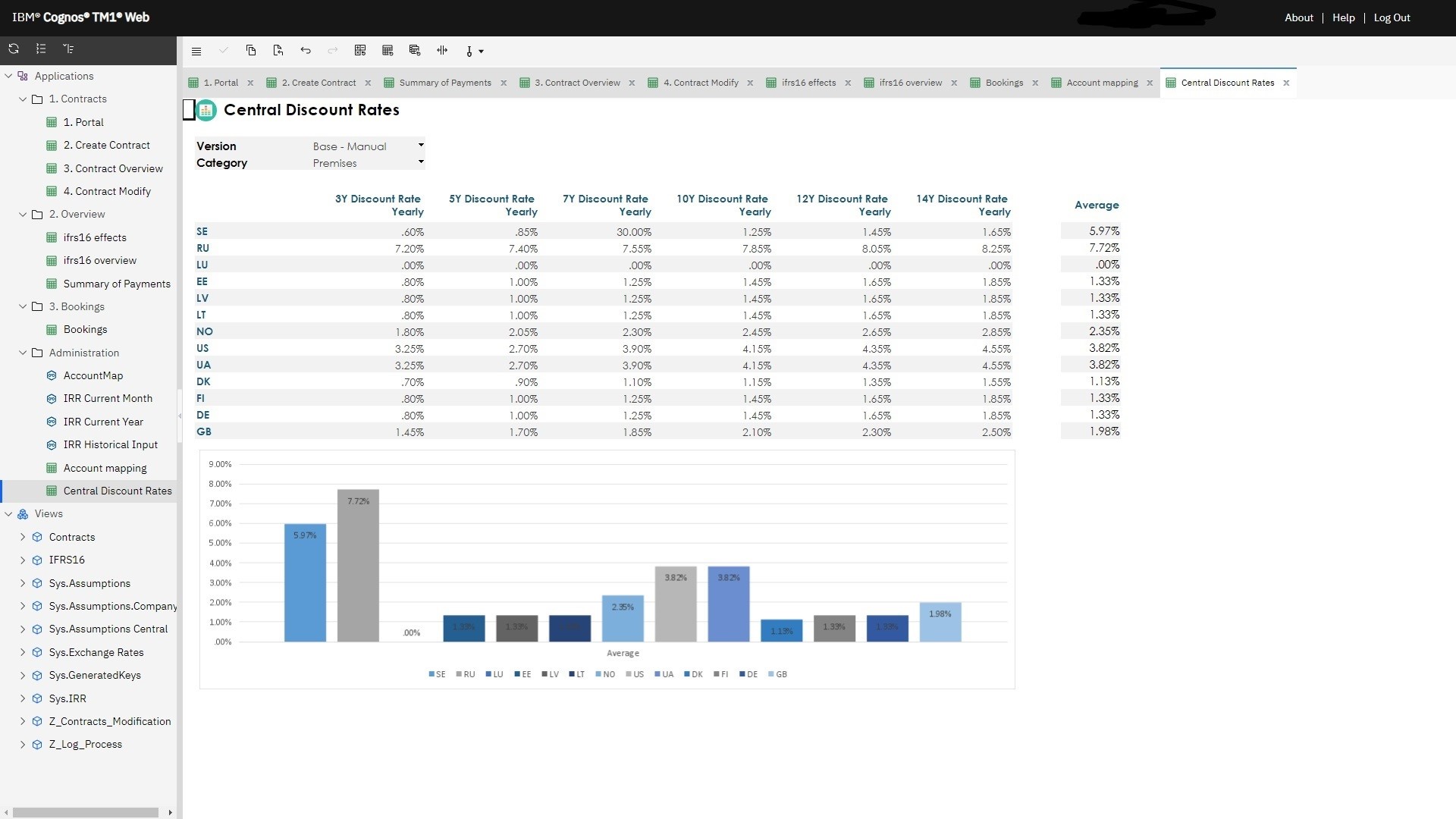

It is possible to import contracts that are settled in currencies other than PLN. We obtain exchange rates and the ratio of PLN to other currencies on a daily basis based on data from the National Bank of Poland. In line with the client's expectations, we create appropriate rules and value conversion logic, thus obtaining the ability to analyze data both in currencies directly related to the contract (contract currency), specific to a given company (local currency) or for the entire group of companies (group currency).

What does the import of contract data into the application look like?

The basic functionality of the application allows you to manually add contracts to the system, but it is also possible to create an appropriate process that imports contract data from an external source, i.e. from a .csv or .xlsx file, as well as in the form of integration with an external data source via Rest API.

Is it possible to export contract and accounting data directly from the application level?

Yes. In the basic version of the application, we adapt the client's process of exporting monthly accounting in the appropriate form of a .csv file, which can then be imported to an external accounting system. At the client's request, we also create additional processes and business logic to export contract data or data directly related to financial calculations.

Does the application allow the use of additional dimensions, parameters and individual data aggregation?

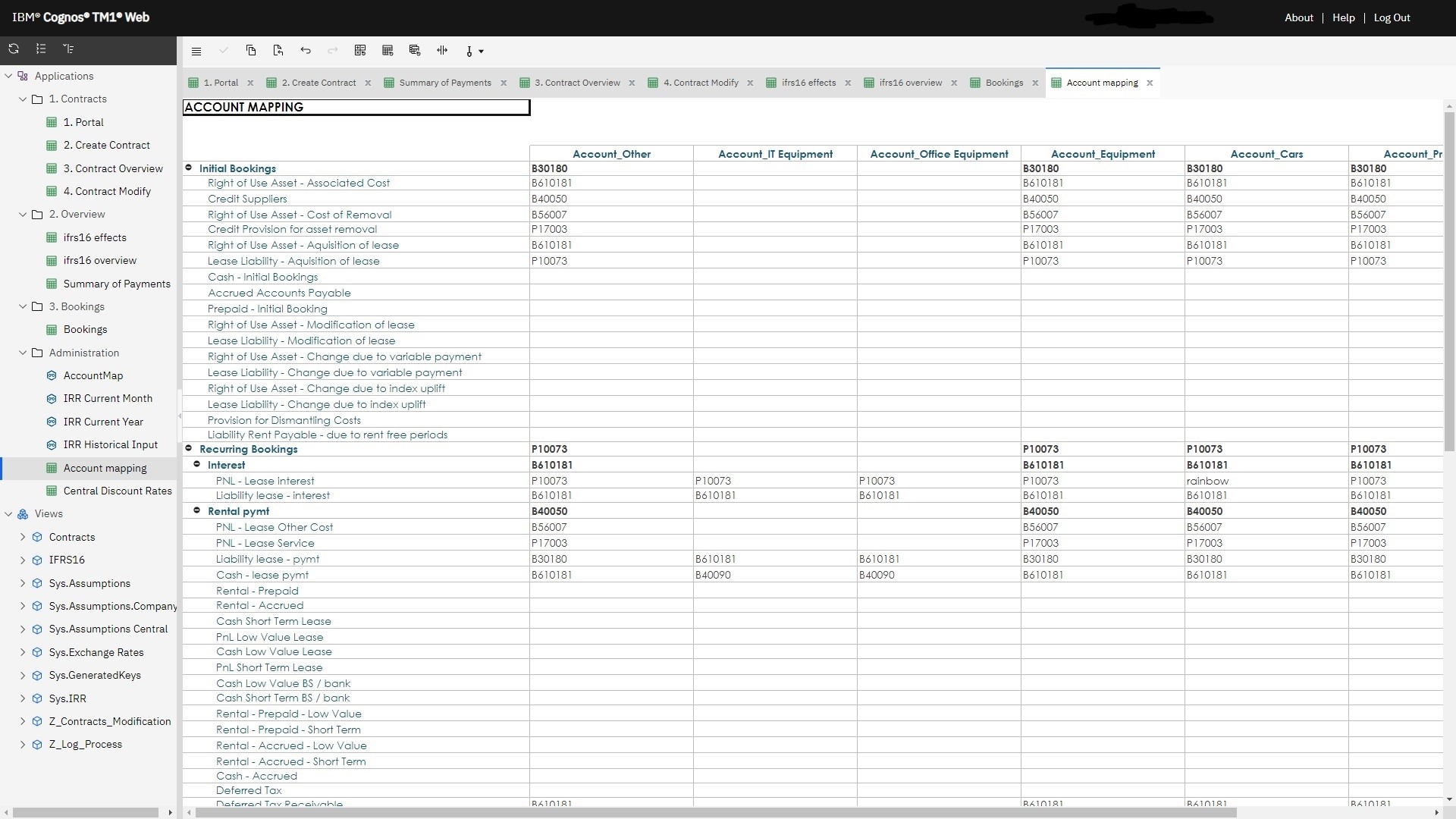

Yes. In line with the client's expectations, the dimensions used in the application are appropriately modified in order to provide the possibility of data analysis in appropriate approaches and aggregations. Depending on the needs, data from additional dimensions or parameters are linked directly to the contract being created or are used as separate elements, which then enable appropriate data analysis, e.g. for contracts from previously matched, specific cost or revenue centers.

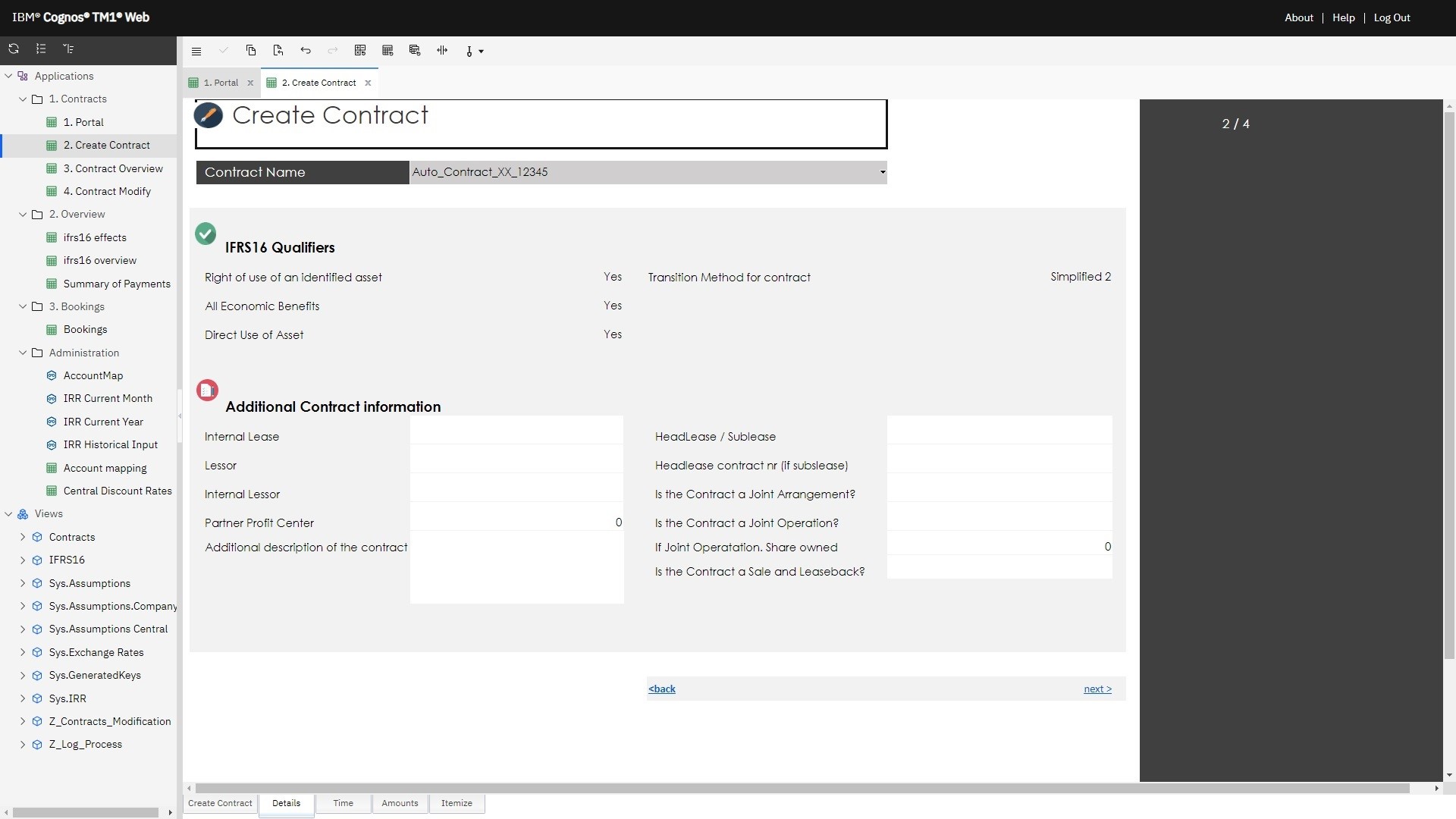

Does the application allow you to create modifications and new versions of contracts due to changes in their parameters?

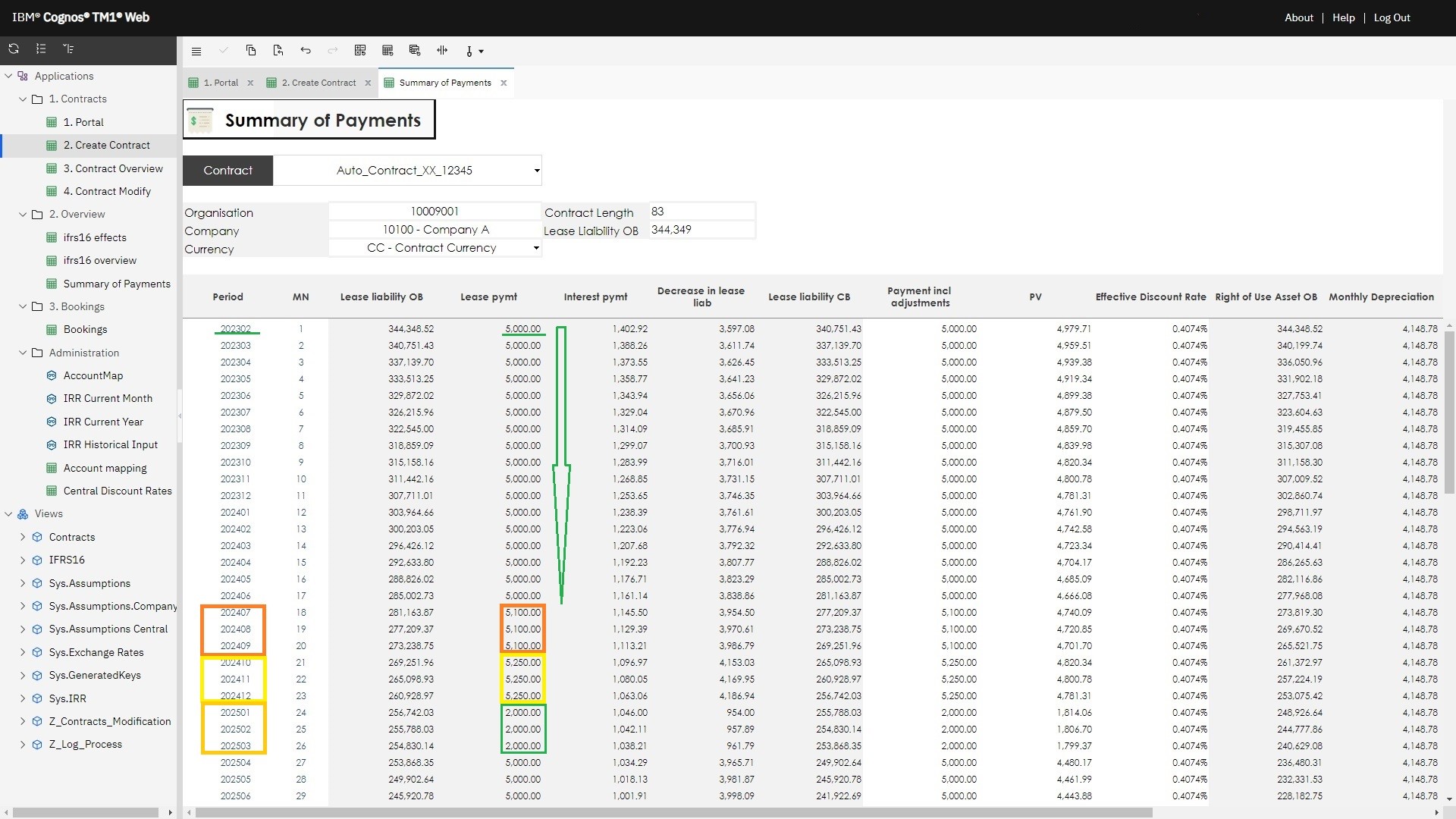

Yes. The ILA16 application allows you to create many modifications to contracts, as well as correct the values of parameters affecting the conversion of individual financial items over time. There is no limit on the number of subsequent versions of contracts - modifications may occur every month. It is also possible to simulate specific situations for a given group of contracts and verify the effects over time.

Is an analysis of the effects on the balance sheet and profit and loss account available?

The calculation in the offered tool is dynamic, i.e. any change in contract parameters (affecting the financial effects) is immediately visible and available on the prepared reports. One of them presents real effects on the balance sheet and profit and loss account after selecting parameters that limit the verified effect, e.g. by entering information about a specific month, company, currency, contract category and elements from previously predefined dimensions.